For insights on optimizing business expenses, explore our guide on cost management strategies. Once costs are broken down, small businesses can assess if any categories are excessive. For example, upgrading to energy-efficient equipment could reduce utilities.

Breaking Down Overhead Costs: Fixed and Variable

- Also, if the rates determined are nowhere close to being accurate, the decisions based on those rates will be inaccurate, too.

- Our mission is to empower readers with the most factual and reliable financial information possible to help them make informed decisions for their individual needs.

- This rate is critical for cost accounting as it helps in predicting the overall expenses related to the production process.

- A predetermined overhead rate is used by businesses to absorb the indirect cost in the cost card of the business.

- Calculating the predetermined overhead rate is crucial for accurate cost accounting and managerial decision-making.

Further, customized input from different departments can be obtained to enhance the accuracy of the budget. It is necessary for operations but does not directly link to creating a product. A high overhead rate can indicate that you need to control your costs better or raise your prices. On the other hand, a low overhead rate might show that you are operating efficiently.

Why You Can Trust Finance Strategists

Using a predetermined overhead rate allows companies to apply manufacturing overhead costs to units produced based on an estimated rate, rather than actual overhead costs. This rate is then used throughout the period and adjusted at year-end if necessary based on actual overhead costs incurred. The overhead rate is calculated by dividing total overhead costs by an appropriate allocation measure such as direct labor hours. A later analysis reveals that the actual amount that should have been assigned to inventory is $48,000, so the $2,000 difference is charged to the cost of goods sold. The allocation base (also known as the activity base or activity driver) can differ depending on the nature of the costs involved.

Step 1: Gather your overhead costs

So, it may not be a good idea with perspective to effective business management. To estimate the level of activity, sales and production budget can be used. However, there is a strong need to constantly update the production level depending on the seasonal fluctuations and the factor affecting the demand of the product. Generally, it can range from 20% to 50% of total costs, depending on the industry.

By factoring in overhead costs in this manner, the company arrives at a more accurate COGS. The key is choosing an appropriate cost driver – like machine hours in manufacturing or headcount in sales – to distribute overhead expenses. Allocating overhead this way provides better visibility into how much overhead each department truly consumes. However, if there is a difference in the total overheads absorbed in the cost card, the difference is accounted for in the financial statement. Let’s understand the detailed perspective of the concept along with steps.

Renegotiating contracts with vendors may yield savings on supplies or services. Suppose following are the details regarding indirect expenses of the business. If a factory is producing some goods, the accountant should determine the number of hours a machine uses during the activity period. Larger organizations tend to employ a different POHR in each department which improves the accuracy of overhead application even though it increases the amount of required accounting labor. The rates aren’t realistic because they are based on accounting estimates.

Further, this rate is calculated by dividing budgeted overheads by the budgeted level of activity. Also, if the rates determined are nowhere close to being accurate, the decisions based on those rates will be inaccurate, too. After reviewing the product cost and consulting with the marketing department, the sales prices were set. The sales price, cost of each product, and resulting gross profit are shown in Figure 6.6. Therefore, the predetermined overhead rate of GHJ Ltd for next year is expected to be $5,000 per machine hour.

It’s a simple process that requires you to gather some data and do a bit of math. Setting overhead budgets and benchmarks for each department also helps control spending. If costs rise above predetermined limits, action can be taken to reduce expenses. Enforcing company-wide cost-saving policies around printing, travel, etc. further helps minimize overhead. This calculates the percentage of indirect costs relative to direct costs.

This comprehensive guide breaks down overhead rate calculation into clear, actionable steps any business can follow. In addition to this, project planning can also be done with the use of an overhead rate. It’s because it’s an estimated rate and can be predicted at the start of the project. Product costing can be extremely helpful in managerial decision-making, and its prime use is related to product costing and job order costing. So, it’s advisable to use different absorption bases for the costing in terms of accuracy. The business is labor-intensive, and the total hours for the period are estimated to be 10,000.

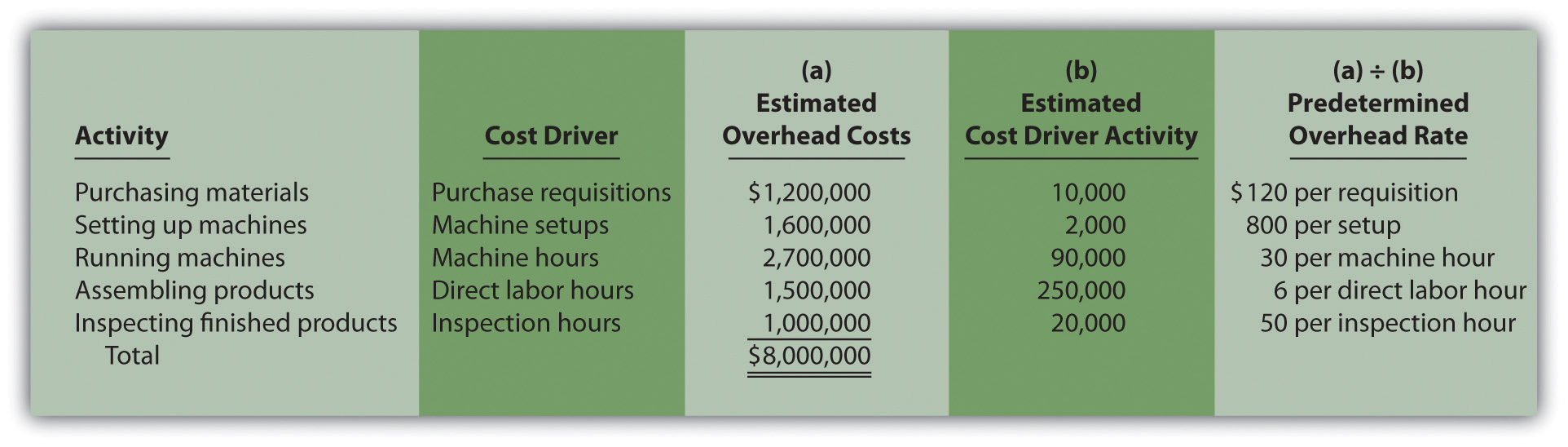

A number of possible allocation bases are available for the denominator, such as direct labor hours, direct labor dollars, and machine hours. Setting accurate predetermined overhead rates aids in better product costing and efficiency in financial operations, ensuring that all production costs are accounted for systematically. Once an overhead rate is freddie mac revolving credit facility calculated using the given formula, it’s absorbed in the cost card of the business using the actual level of the activity. At the end of the accounting period, the actual indirect cost is obtained and compared with the absorbed indirect. A predetermined overhead rate is used by businesses to absorb the indirect cost in the cost card of the business.